A small business is always in need of funds when it comes to working on business expansion and growth. A business term loan provides SMEs the option to benefit from new opportunities to capture additional ROI. Term loans are the closest product to conventional bank loans, and quite frankly, this option is cheaper (most times) than other alternative working capital loans (MCA’s).

Applying for a traditional loan from a bank can be a very challenging process, but today, small businesses can utilize other alternatives. Lenders offer a wide array of financing products, but every business must carefully analyze its options before applying for any loan.

As mentioned briefly above, a term loan is a classical definition of a business loan. This type of financing comes in different variables: a short-term loan, a mid-term loan, or a long-term loan. A term loan provider gives you access to capital upfront for business purposes. Once you have been given the loan, you start to repay it over a set period with fixed and equal payments.

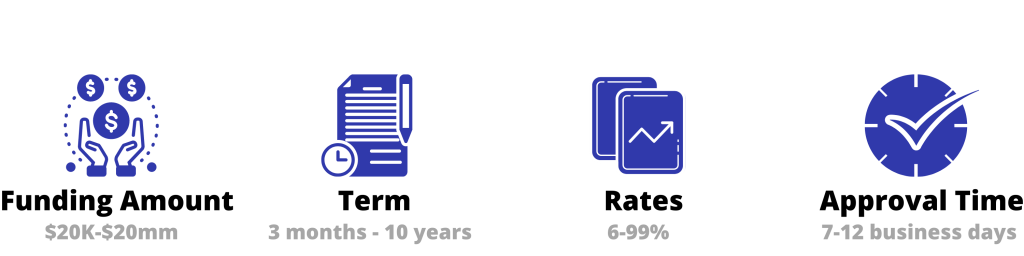

For this, interest rates start from 6% up to 99%. The repayment period varies between 3 months to 5 years with online lenders and up to 10 years with traditional banks. The funding amount you can qualify for ranges between $5k to $5 million. However, requirements and rates vary greatly between different banks and lenders. The rates and terms mostly depend on a few main factors; credit score, annual revenue, time in business, and profitability.

Small business loans can help you, but the question is, what is the most suitable type of loan for you? The main differences between a business term loan and a business line of credit are the repayment period and the intended use of funds.

With a business term loan, you get access to a lump sum of cash. Then, you start repaying the loan with a fixed monthly payment right away, even if you have not used the funds just yet.

A term loan is a better fit for businesses looking to buy an expensive piece of equipment or to purchase additional inventory. Unlike term loans, a business line of credit provides you with an ongoing pool of funds. This means that you can use the funds repeatedly whenever the balance is cleared in full. With this type of financing, you can withdraw a portion of the cash and pay the interest plus fees on the specific amount borrowed.

If you’re looking for working capital with a prime rate and relatively quick funding process to other loans, a term loan is probably an ideal option for you. However, this type of financing has some requirements that you will have to meet.

To become eligible for a business term loan involves multiple factors. What matters for lenders is your time as a business in the industry, credit score, and the annual revenue of your company. Usually, a term loan offers better rates and longer periods than other working capital loans. As a result, qualifying for a term loan can be more challenging due to stricter qualifying requirements.

Merchant cash advance is a working capital solution that provides your business with a sum of cash in exchange for a portion of future receivables.

Invoice factoring designed to provide you with instant access to fast cash in exchange for invoices. That cash can be used for a marketing campaign or any other urgent need.

An equipment loan can help you acquire physical assets for your business with a low down payment. This alternative fits businesses that are looking to upgrade their equipment.

A business term loan provides you a sum of capital that you pay back with fixed, equal monthly payments over a set repayment period.

SBA loans are partially guaranteed by the U.S. Small Business Administration and provided by traditional banks, online lenders and credit unions.