As a small business owner, you might have thought of replacing your business equipment. Equipment financing products can help you purchase new or used equipment. Unlike other business loans, the asset you purchased will serve as collateral.

In its simplest terms, equipment financing is a form of a business loan that is used to secure fixed assets. An equipment financing loan provider gives you a loan with a fixed monthly repayment term to purchase new or used equipment.

Heavy machinery, trucks, construction equipment, staffing, and IT equipment are the most common types of equipment financed.

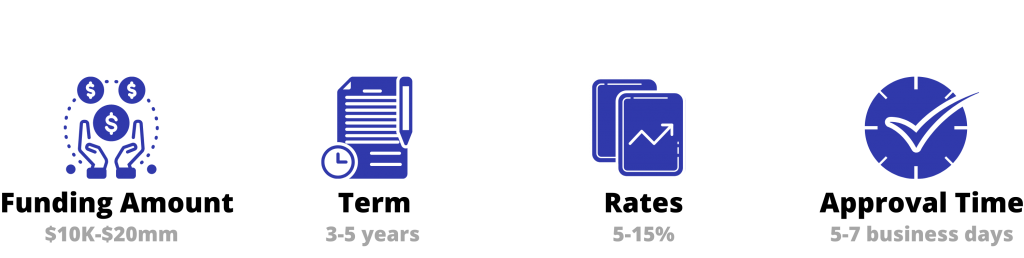

With equipment financing, the loan amount is based on the value of the equipment. Purchasing hard assets can be costly. Although a down payment of 10-20%is typically required, this way, equipment financing may still save you from using a significant portion of your capital.

Unlike invoice factoring or merchant cash advances, equipment financing has a fixed repayment structure. You make a fixed payment every month, which is the principal amount + interest over a set period.

Before the lender grants you this type of loan, the condition of the equipment is inspected. In case of a default, the asset you purchased will serve as “insurance.” Therefore, the business lender wants to make sure that the equipment has a resale value.

Let’s assume you wanted to purchase an industrial machine that costs $100,000. It can pack thousands of bags and save you the cost of manpower. After you negotiated with the lender, you received a 6-year term at 6% secured against the machine. Once the loan is paid in full, you own the equipment free of any lien.

Equipment leasing is for the use of the asset during the repayment period. At the end of the term, you’ll have three choices to make; resuming the lease, unloading the asset, or purchasing the asset. After the loan is paid in full, the equipment will remain in your business’ possession. To finance the equipment will be a better option in case you are planning to use the equipment for the long term.

Equipment leasing is more suitable for small businesses that replace their equipment frequently. One of the advantages of leasing is that leasing is a form of “off-balance-sheet” product that can help you to reduce your liabilities.

Using equipment loans to purchase hard assets allows businesses to preserve cash for potential expenses such as payroll, inventory, taxes, new contracts, or other unexpected business expenses.

Using a loan to buy expensive assets can increase the purchasing power of your business. However, the equipment you just purchased may increase your liabilities.

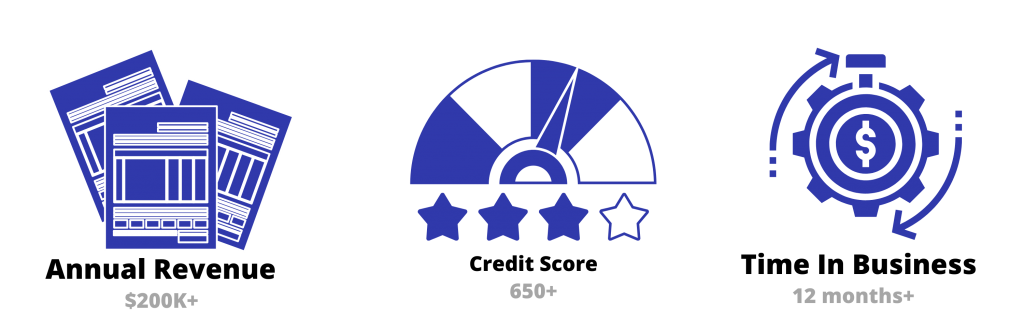

Many small businesses will want to use this option to acquire hard assets, but lenders are usually more cautious with this type of loan. Typically, lenders require at least a year in business, at least $100K in annual revenue and a 600+ credit score. Thanks to the collateral, bad credit will not automatically disqualify you from getting an equipment loan.

The best industries for Equipment Loans

Merchant cash advance is a working capital solution that provides your business with a sum of cash in exchange for a portion of future receivables.

Invoice factoring designed to provide you with instant access to fast cash in exchange for invoices. That cash can be used for a marketing campaign or any other urgent need.

An equipment loan can help you acquire physical assets for your business with a low down payment. This alternative fits businesses that are looking to upgrade their equipment.

A business term loan provides you a sum of capital that you pay back with fixed, equal monthly payments over a set repayment period.

SBA loans are partially guaranteed by the U.S. Small Business Administration and provided by traditional banks, online lenders and credit unions.